The author would like to thank Vidushan Ragukaran and Ari Rajendra for their contributions to this blog.

The 2024 World Economic Forum (WEF) that took place at Davos-Klosters in mid-January attracted over 60 heads of state and government leaders. There was a consistent emphasis on AI and cybersecurity risk governance, a renewed focus on the energy transition for environmental concerns and a noticeable discussion around prioritizing women’s health for social advancement. Below, we highlight the key takeaways.

AI, Risks and Governance

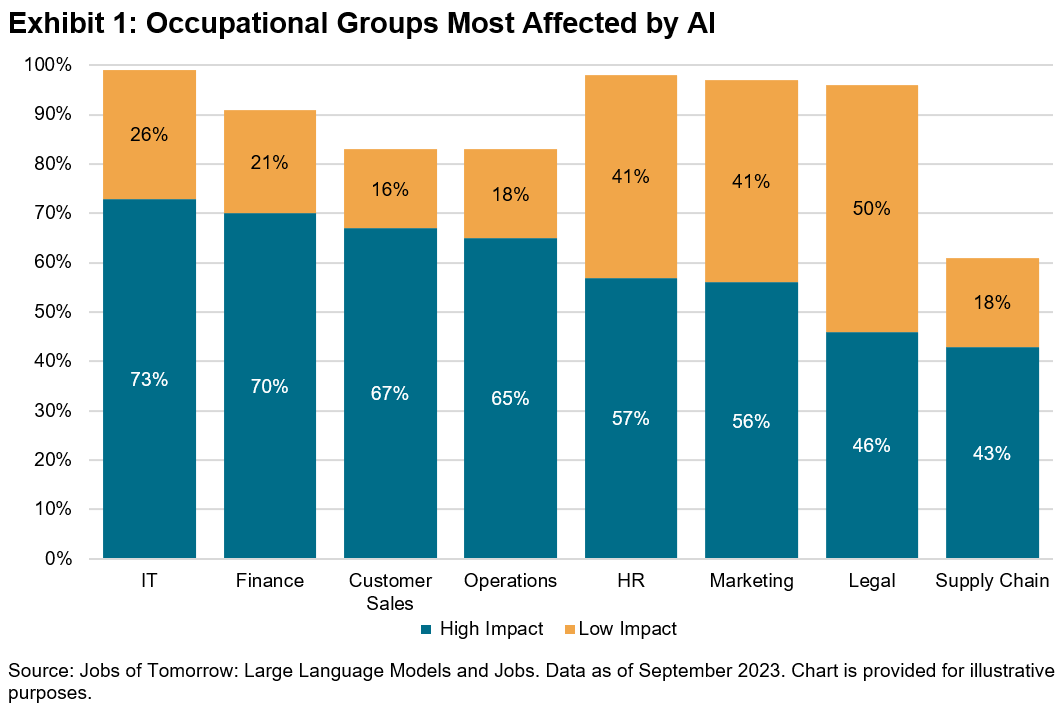

The key theme at the WEF’s Annual Meeting was the role of artificial intelligence in driving economic and societal progress1 and a growing need to explore how AI can bring transformations to business operations and performance. Exhibit 1 shows the result of an analysis of over 19,000 individual tasks across 867 occupations.2

Additionally, AI can also potentially assist in addressing challenges in healthcare, agriculture and climate change. An example is its use in a UN initiative aiding climate-vulnerable communities in Burundi, Chad and Sudan, where AI is used to try to predict weather patterns to enable better planning for local communities.3

Featured S&P DJI Index: S&P Kensho Global Artificial Intelligence Enablers Index – seeks to track global companies that develop the technology, infrastructure and services propelling AI growth.

Other S&P DJI Indices: S&P Kensho AI Enablers Index, S&P Kensho Artificial Intelligence Enablers & Adopters Index

AI offers the potential to address worldwide challenges, but it is also necessary to establish safeguards in connection with that growth. The increased adoption of AI requires greater cybersecurity protection and the establishment of ethical governance frameworks.4

Featured S&P DJI Index: S&P Kensho Cyber Security Index – seeks to track innovative companies delivering cybersecurity solutions.

Other S&P DJI Indices: S&P Global Semiconductor Index, Dow Jones U.S. Semiconductors Index

Sustainability with a Focus on Equitable Energy Transition

The Equitable Transition Initiative created at the WEF seeks to promote an environmentally conscious transition with a focus on economic fairness.5 The initiative aims to evaluate the effects of climate mitigation measures on individuals, encouraging opportunity optimization and risk mitigation. Central topics include investing in renewables, energy efficiency and innovative storage technologies.

The energy transition was also recently discussed at COP28, emphasizing the need to accelerate the transition to clean energy to achieve the 1.5°C goal. Over 130 nations pledged to triple global renewable energy capacity to 11,000GW and double energy efficiency by 2030—a historic shift from fossil fuels.

Featured S&P DJI Index: S&P Global Clean Energy Index – seeks to track businesses in developed and emerging markets that are highly aligned towards the provision of clean energy, thus capturing the energy transition as it takes place globally.

Other S&P DJI Indices: S&P Global Clean Energy Select Index, S&P Kensho Clean Energy Index, S&P Kensho Clean Power Index, S&P Kensho Cleantech Index, S&P Global Essential Metals Producers Index

Healthcare with a Focus on Women’s Health and Digital Healthcare

Another key point mentioned at WEF is healthcare. A WEF report suggests addressing women’s health challenges could add at least USD1 trillion to the global economy by 2040, potentially resulting in a 1.7% increase in per capita GDP by improving well-being and increasing workforce participation.6 The Forum’s newly established Global Alliance for Women’s Health has support from 42 organizations, dedicated to enhancing women’s health globally, and it has secured a financial commitment.

Featured S&P DJI Index: S&P Kensho Digital Health Index – seeks to track companies specializing in remote healthcare delivery, whose services could help address the challenge in women’s health.

In conclusion, we are seeing increased recognition of AI applications and their risks, the urgency of energy transition and the opportunity in women’s health. S&P DJI offers additional indexing solutions to capture the opportunities and address upcoming challenges.

1 Pomeroy, R. and Myers, J. (2024) AI – artificial intelligence – at Davos 2024: What to know, World Economic Forum. Available at: https://www.weforum.org/agenda/2024/01/artificial-intelligence-ai-innovation-technology-davos-2024/.

2 World Economic Forum In Collaboration with Accenture (2023) Jobs of tomorrow: Large language models and jobs -weforum.org, World Economic Forum. Available at: https://www3.weforum.org/docs/WEF_Jobs_of_Tomorrow_Generative_AI_2023.pdf.

3 Masterson, V. (2024) 8 ways AI is helping tackle climate change, World Economic Forum. Available at: https://www.weforum.org/agenda/2024/01/ai-combat-climate-change/.

4 Palma, B. (2024) Ai Is Transforming Cybersecurity: How can security experts respond?, World Economic Forum. Available at: https://www.weforum.org/agenda/2024/01/arms-race-cybersecurity-ai/.

5 World Economic Forum (2024) World Economic Forum annual meeting 2024, BusinessGhana. Available at: https://www.businessghana.com/site/events/other-events/476406/World-Economic-Forum-Annual-Meeting-2024.

6 World Economic Forum (2024a) New Global Alliance for Women’s health could help boost global economy by $1 trillion annually by 2040, World Economic Forum. Available at: https://www.weforum.org/press/2024/01/wef24-new-global-alliance-for-womens-health-could-boost-global-economy-by-1-trillion-annually-by-2040/.

The posts on this blog are opinions, not advice. Please read our Disclaimers.