In September 2022, S&P DJI was pleased to add the S&P Sector-Neutral High Yield Dividend Aristocrats® to the S&P Dividend Aristocrats Index Series. While most dividend indices have notable sector under- and overweights versus their underlying benchmark, this index is the first in the series to be sector neutral. As such, this index emphasizes dividend growth and high yield while keeping the same sector weights as its benchmark, the S&P Composite 1500®. In this blog, we will review the methodology of this index and explain how it may serve as a more balanced dividend growth strategy that is more closely aligned with its benchmark.

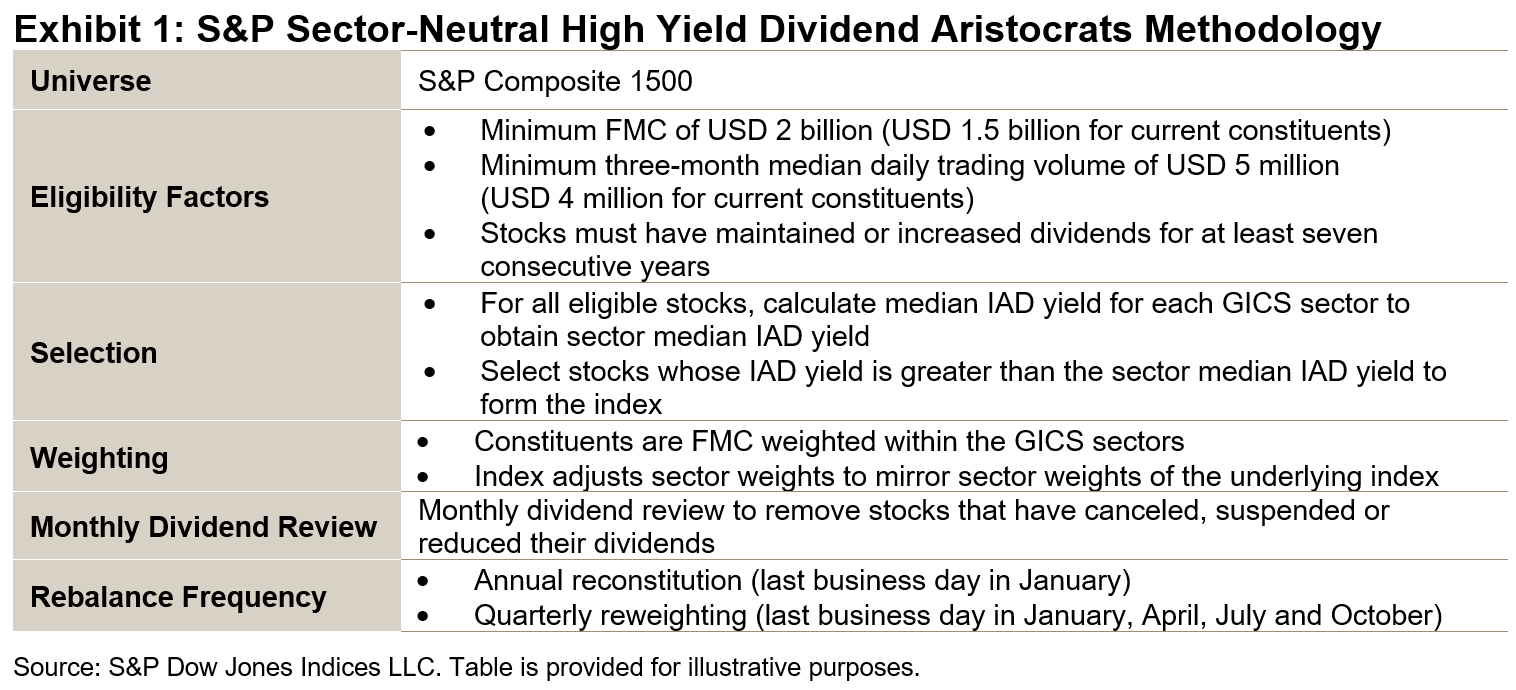

Exhibit 1 summarizes the methodology construction of the S&P Sector-Neutral High Yield Dividend Aristocrats. A hallmark of the S&P Dividend Aristocrats Indices is the dividend growth requirement, which typically requires constituents to raise their total dividend per share every year for a minimum number of years. To facilitate sector-neutrality in this index, the minimum was set at seven years of stable or growing dividends. This threshold ensures that enough constituents from each sector qualify, while incorporating many of the desired characteristics of a dividend growth strategy.

Companies that meet the dividend growth requirement must also have an indicated annual dividend (IAD) yield that is greater than the sector median yield. Constituents are weighted by float market cap (FMC) within the GICS® sectors. To incorporate sector-neutrality, the index adjusts the sector weights to mirror the sector weights of the S&P Composite 1500.

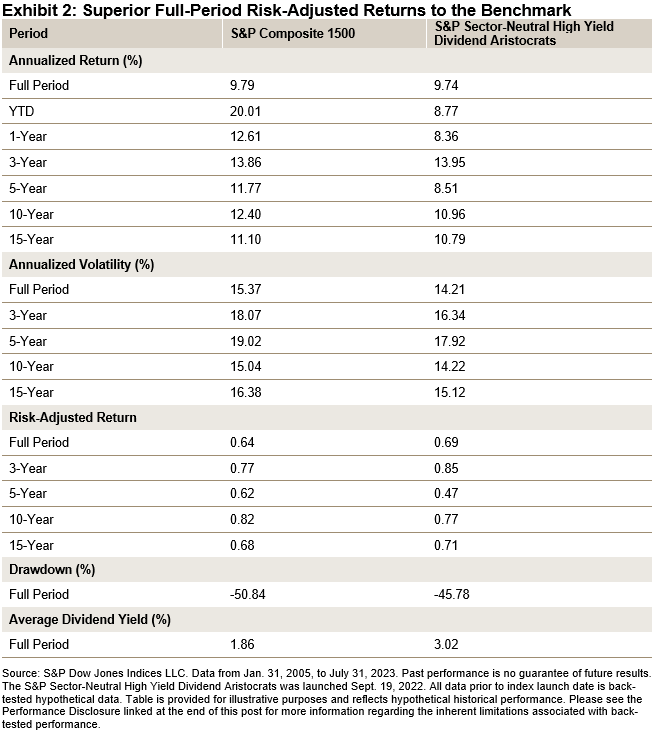

As Exhibit 2 shows, the index’s absolute performance versus the benchmark has been almost identical since its first value date (Jan. 31, 2005). Importantly, however, the S&P Sector-Neutral High Yield Dividend Aristocrats has exhibited lower volatility relative to the benchmark, leading to superior risk-adjusted returns. Additionally, the maximum drawdown over the period was approximately 5% lower.

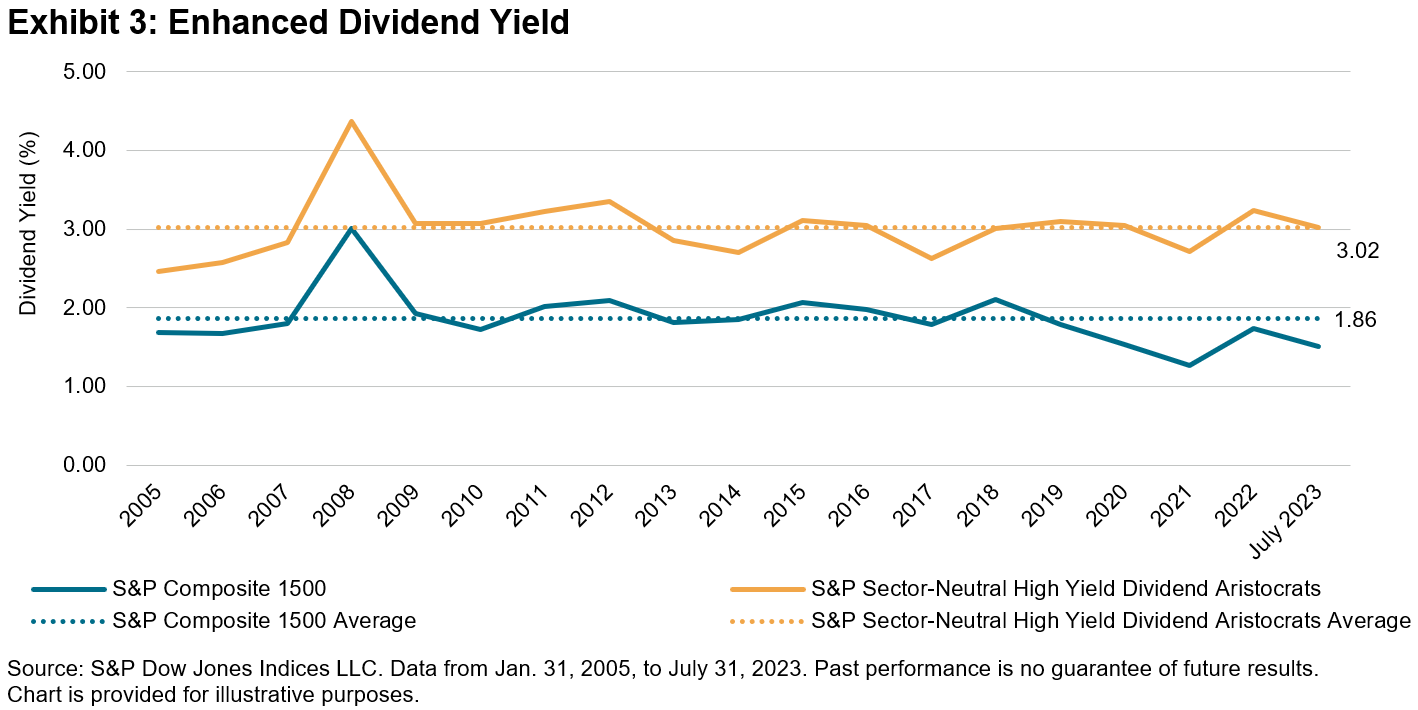

As Exhibit 3 shows, the index’s dividend yield has been larger than the S&P Composite 1500 every year since 2005. Furthermore, the average dividend yield for the S&P Sector-Neutral High Yield Dividend Aristocrats was 3.02% versus 1.86% for the benchmark over the same period. The significant uptick in dividend yield is a positive result of the index only selecting constituents whose IAD yield is greater than the sector median IAD yield.

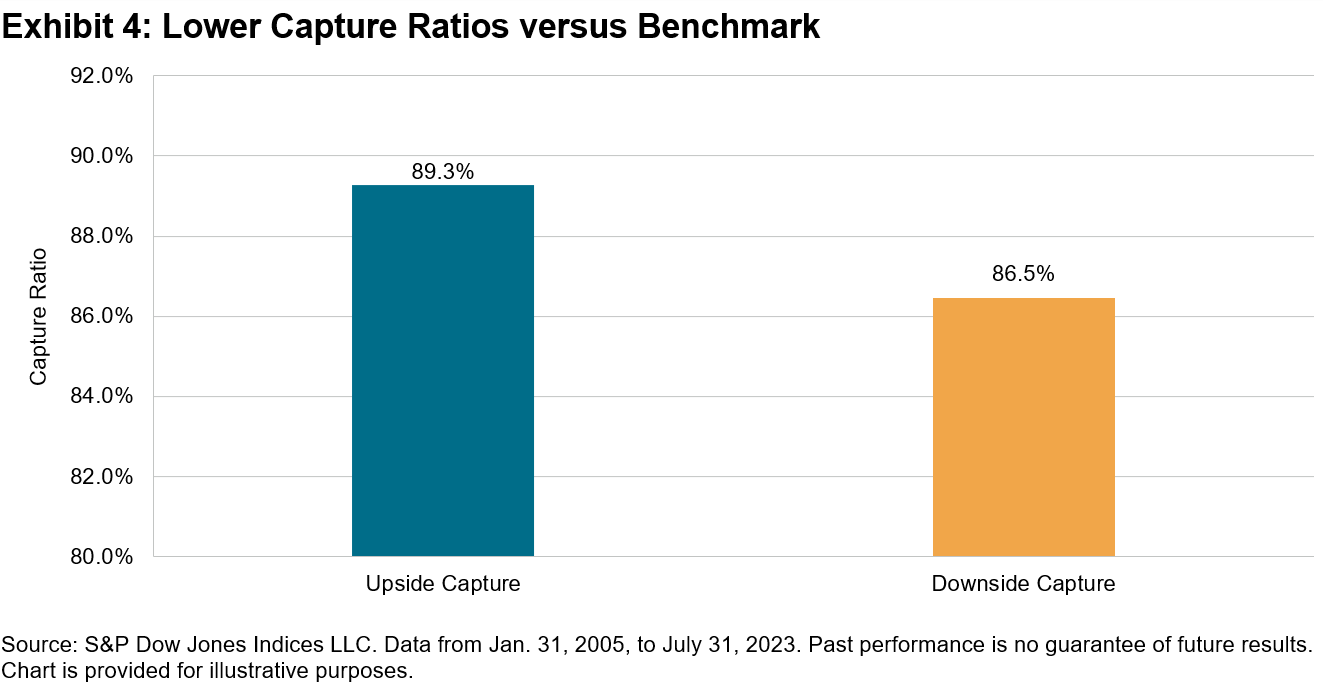

As Exhibit 4 shows, the index has historically provided downside protection relative to the S&P Composite 1500, exhibiting an 86.5% downside capture ratio. This metric supports the notion that the S&P Dividend Aristocrats methodology provides stability since the ability to consistently maintain or grow dividends every year through different economic environments can be an indication of financial strength and discipline.

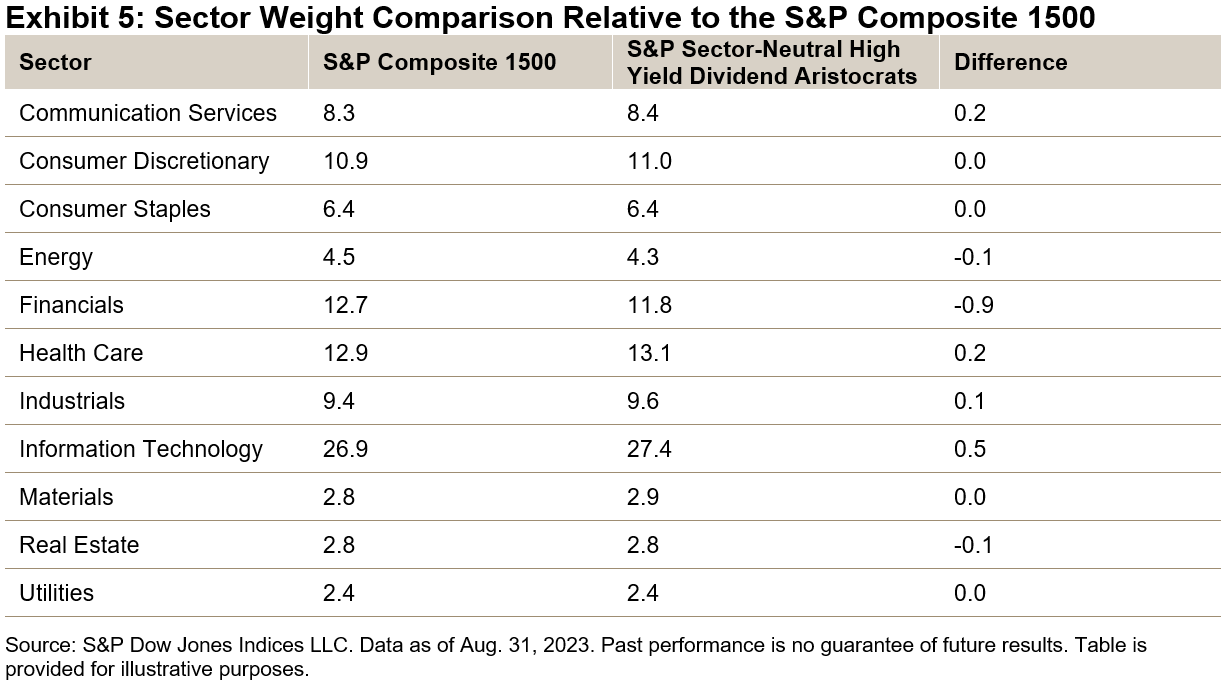

Exhibit 5 highlights the considerable similarity in sector weights due to the sector-neutral approach implemented in the methodology. Small deviations in sector weights can be expected due to constituent performance within the sectors between reweightings.

Historically, the S&P Sector-Neutral High Yield Dividend Aristocrats has had comparable returns and sector weights relative to its benchmark, while also providing enhanced dividend yields and downside protection. For investors seeking a balanced dividend strategy focused both on dividend growth and yield, the S&P Sector Neutral High Yield Dividend Aristocrats is a compelling option to consider.

The posts on this blog are opinions, not advice. Please read our Disclaimers.