Dividends are becoming increasingly important as investors grapple with higher U.S. Treasury yields that do not appear to be going down anytime soon. However, not all dividend markets are created equal. Below are four charts that compare dividend index performance in Asia to the U.S.

The S&P Pan Asia Dividend Aristocrats Index brings S&P Dow Jones Indices’ notable “Dividend Aristocrats®” index methodology to Asia. The index selects companies in both emerging and developed Asian economies that have increased their dividends every year for at least the past seven years. Please click here for the full index methodology and here for more dividend-related research from KraneShares.

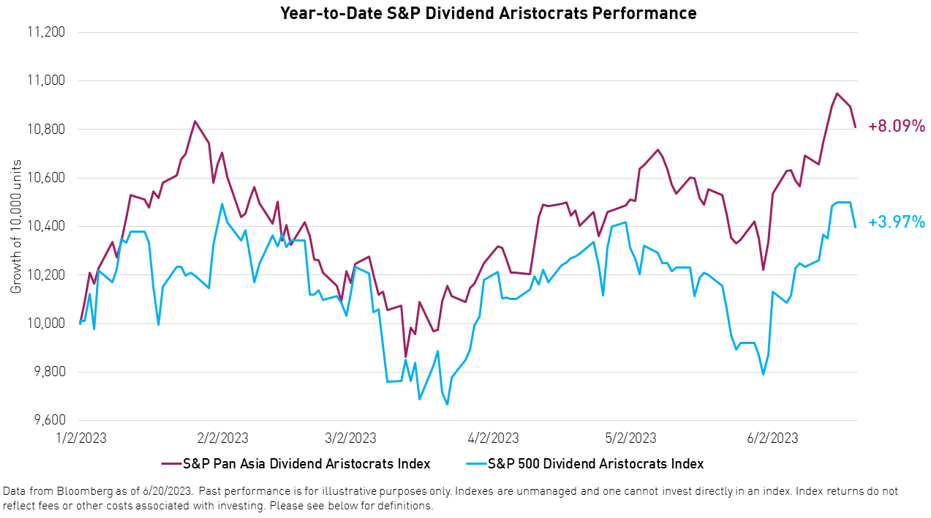

1. Momentum

The S&P Pan Asia Dividend Aristocrats Index has outperformed the S&P 500® Dividend Aristocrats Index, which tracks dividend growers in the U.S., so far this year, gaining 8.09% versus 3.97% for its U.S. counterpart, as of June 20, 2023.

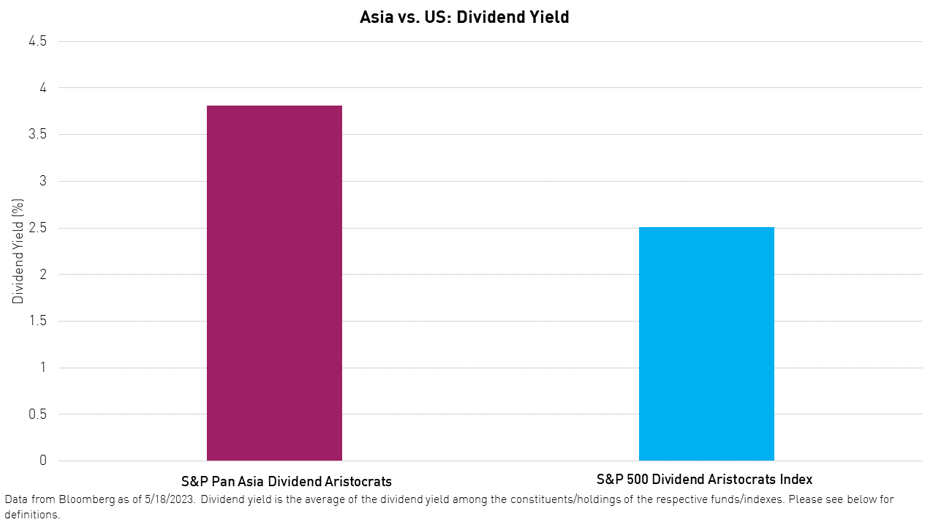

2. Yield

S&P Pan Asia Dividend Aristocrats Index constituents also currently offer a higher dividend yield, on average, than their U.S. counterparts.

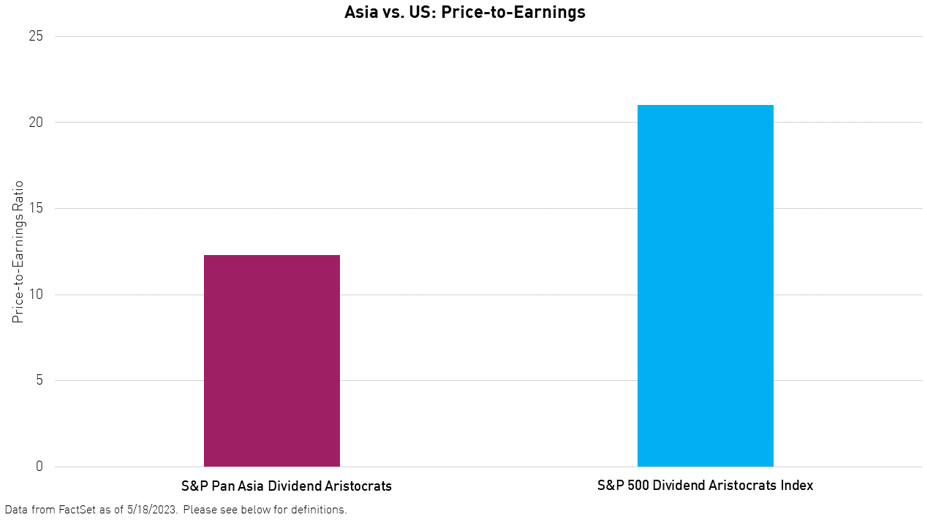

3. Valuation

S&P Pan Asia Dividend Aristocrats Index constituents are currently trading at nearly one half of the price-to-earnings multiple of their U.S. counterparts, on average.

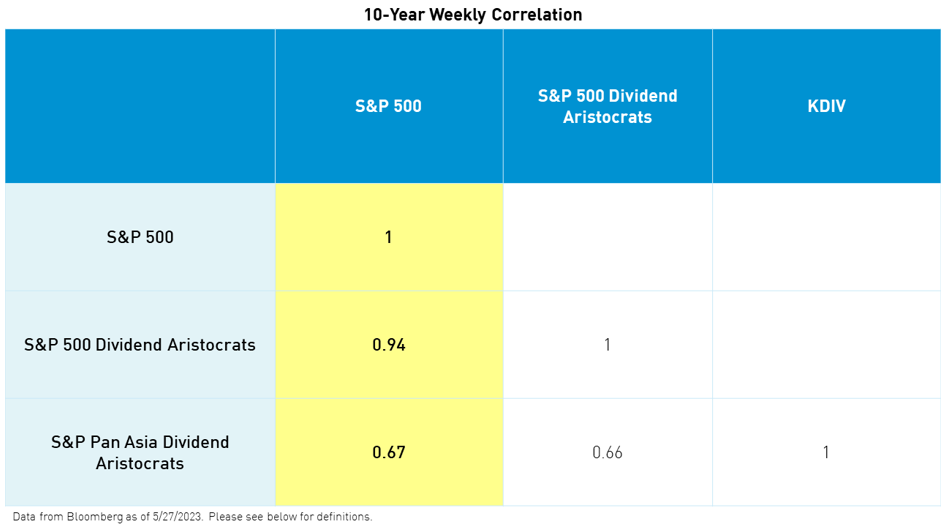

4. Correlation

S&P Pan Asia Dividend Aristocrats constituents have also exhibited relatively low correlations to the broad U.S. equity market and the S&P 500 Dividend Aristocrats Index constituents, which may present additional portfolio benefits over the long term.

Definitions:

S&P 500 Dividend Aristocrats Index: The S&P 500 Dividend Aristocrats Index measures the performance of S&P 500 companies that have increased their dividends every year for the last 25 consecutive years. The index treats each constituent as a distinct investment opportunity without regard to its size by equally weighting each company. The index was launched on May 2, 2005. See full methodology here.

S&P Pan Asia Dividend Aristocrats Index: The S&P Pan Asia Dividend Aristocrats Index measures the performance of constituents within the S&P Pan Asia Broad Market Index (BMI) that have followed a policy of consistently increasing dividends every year for at least seven years. The index was launched on April 14, 2009.

S&P 500: The S&P 500 is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 9.9 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 3.4 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization. The index was launched on March 4, 1957.

S&P Pan Asia Broad Market Index (BMI): The S&P Pan Asia BMI is a sub-index of the S&P Global BMI and a comprehensive benchmark including securities from developed and emerging Asia. The index was launched on Dec. 31, 1997.

Dividend Yield: The percentage of a company’s share price that said company pays out in dividends each year.

Price-to-Earnings Ratio (P/E): A measure of whether a company is over or under-valued. P/E is calculated as a company’s price per share divided by its earnings per share.

Earnings Per Share (EPS): The total revenue of a company divided by the number of shares outstanding.

Correlation: Correlation is a statistic that measures the degree to which two securities move in relation to one another. Correlations are shown here as the correlation coefficient, which is a value that must fall between -1 (inverse correlation) to 1 (absolute correlation).

The S&P 500®, S&P 500 Dividend Aristocrats Index, S&P Pan Asia Dividend Aristocrats Index and S&P Pan Asia Broad Market Index are products of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”). S&P®, S&P 500®, Dividend Aristocrats® are trademarks of S&P Global, Inc. or its affiliates (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Kraneshares ETFs based on SPDJI’s indices are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates or licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions or interruptions of the Indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.