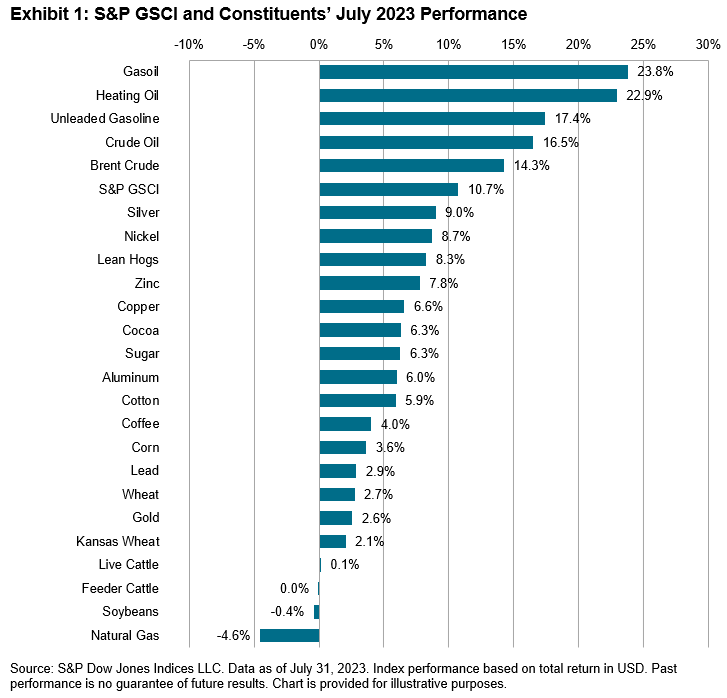

The S&P GSCI, the broad commodities benchmark, started the second half of the year in a blistering heat wave and rose 11% on the back of petroleum commodities, which all increased by more than 14% in July. The remaining four sectors within the S&P GSCI also rose during the month, as fears of a recession abated with inflation falling and the Fed possibly getting close to ending their rate hiking cycle. Strong inflows into commodity ETFs and the covering of short positions across individual commodities helped to create a potential bottom in a few key commodities futures markets.

The energy sector completely reversed its underperformance from the first half of the year, bringing all commodities into positive territory for 2023. OPEC+ production cuts and the absence of negative economic data helped to lift the fossil-fuel-based commodities in July. Demand for petroleum has remained strong during the energy transition, as the world continues to rely on old ways to fuel the economy, as can be seen by strong import demand across nations, particularly in Asia. The S&P GSCI Gasoil and the S&P GSCI Heating Oil were the standouts for the month, rising 23.8% and 22.9%, respectively.

The S&P GSCI Industrial Metals rose 6.5% with all five of the top-traded metals rising in July. For the past few months, Commodity Trading Advisors (CTAs) had large short positions in the space, but short covering in July led to a strong bounce off the lows for several key metals, which have posted some of the worst YTD performance rates in the commodities markets.

Another source of positive news came from the precious metals sector. The S&P GSCI Gold was up 8.1% YTD, as market participants positioned for future U.S. dollar weakness with expectations for the Fed to end their rate hiking cycle soon. Central banks across the globe have increased their gold reserves recently at a pace not seen in years, which typically prefaces a rise in gold prices. The S&P GSCI Silver joined the party by rising 9.0% in July and moving into positive territory for the year. This typically happens as silver tends to track gold moves higher, but with a lag.

The S&P GSCI Agriculture grew by a modest 3.0%, while the S&P GSCI Wheat and the S&P GSCI Corn rose the most as concerns over the latest crop yields were prominent. A recent S&P Global post highlighted the potential for China to have reached peak food demand. China is the biggest consumer of grains globally, but the World Bank recently forecasted that after decades of strong growth, their population will fall by 80 million people over the next 25 years. Could this lead to less demand, or will new areas of demand, such as in more environmentally friendly biofuels, spur new global consumption to supplant the drop in the food needs of China over time?

The posts on this blog are opinions, not advice. Please read our Disclaimers.