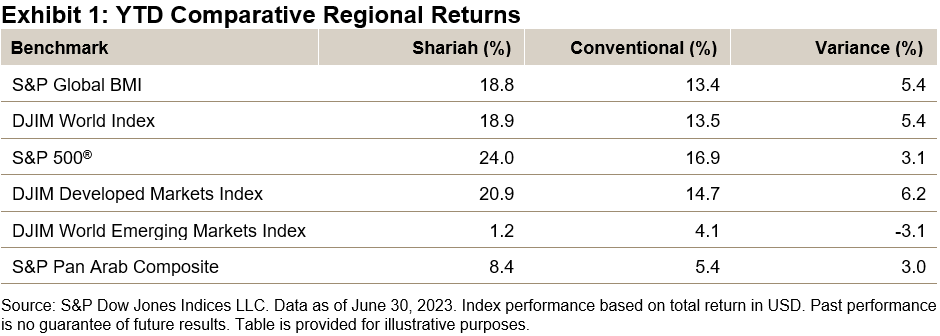

The iBoxx Sovereign Debt Indices span developed and emerging markets, including the iBoxx Global Government Index (GGI), iBoxx Eurozone, iBoxx USD Emerging Markets Sovereigns and iBoxx Global Emerging Market Index (GMEX) series.

Interest in government debt has increased since last year, following the “run-to-quality” amid the 2022 markets’ rout and the shift to a higher interest rate environment, which made sovereign yields attractive again.

At the same time, with sustainability considerations becoming mainstream, especially in Europe, the demand for sovereign ESG solutions has also picked up. Given the importance and the size of the sovereign debt market, sustainability benchmarks still have a lot of room to grow.

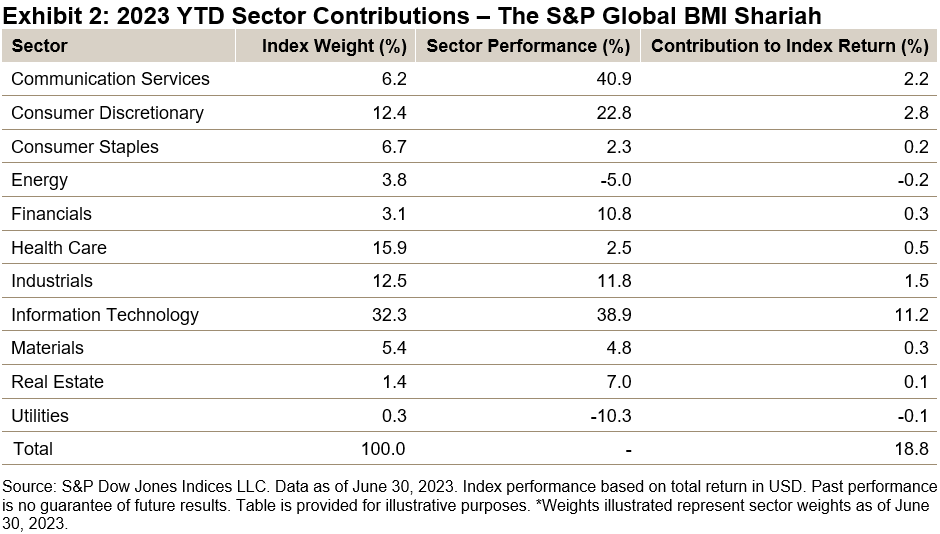

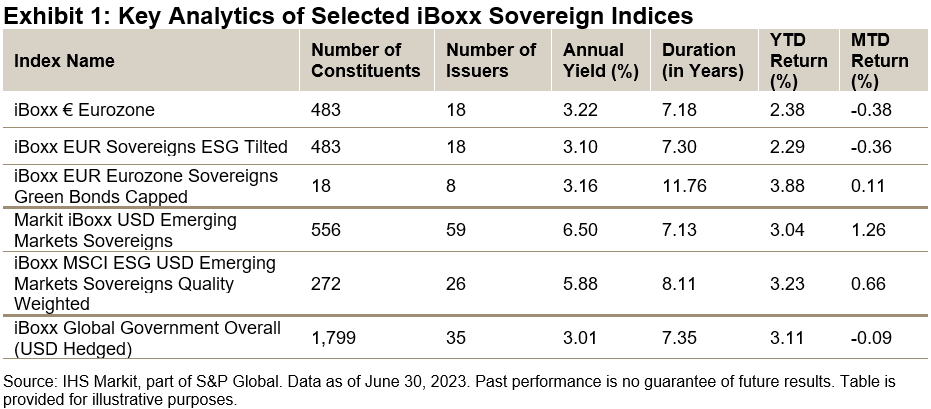

The iBoxx Indices shown in Exhibit 1 show three examples of different index solutions to approach government debt with a sustainability overlay. Exhibit 1 summarizes their key statistics and compares them to broad benchmarks.

Developed Markets: Eurozone Exposure

Firstly, the iBoxx EUR Sovereigns ESG Tilted Index reflects exposure to the eurozone government debt market by overweighing countries with a positive ESG score1 and excluding nations in the very high risk category. In addition, only countries that are considered “free” or “partially free” by Freedom House2 are included. The final composition gives higher weights to countries with favorable Sustainalytics country-risk scores.

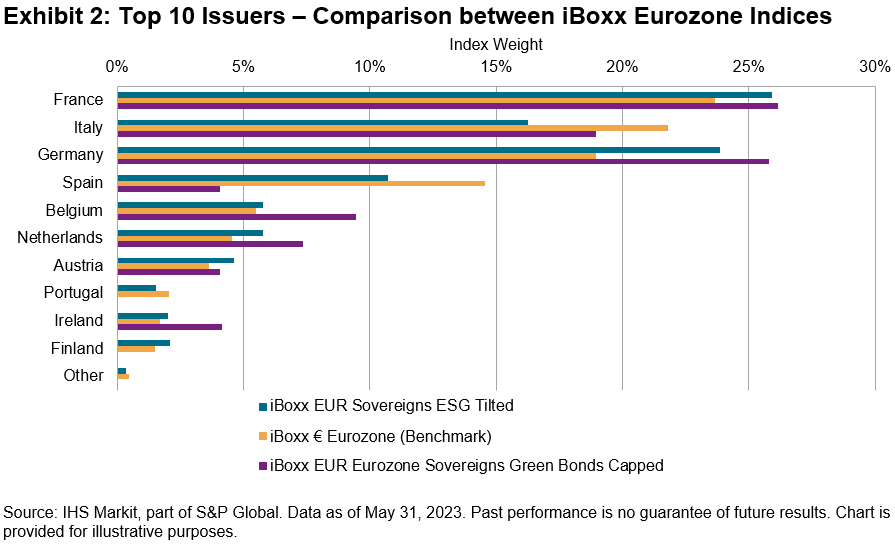

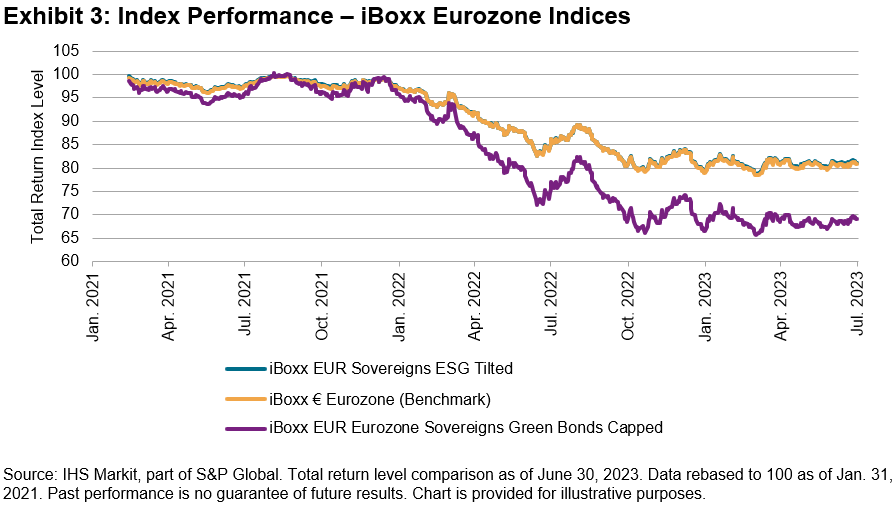

On the other hand, the iBoxx EUR Eurozone Sovereigns Green Bonds Capped Index uses a different approach altogether. While still providing exposure to the eurozone debt market, the sustainability overlay focuses on impact, rather than risk, with constituents limited to green bonds only. After being formed by supranationals, the green bond market then became dominated by corporate issuers, and we are now seeing a steady increase in sovereign green bonds. As per their definition, green bonds must be issued with the Use of Proceeds (UoP) earmarked for environmentally friendly projects. The iBoxx solution leverages the Climate Bond Initiative’s (CBI)3 green bonds database, which uses a proprietary taxonomy aligned with the Paris decarbonization trajectory. Bonds included in the benchmark cover investment grade sovereign issuers with a minimum amount outstanding of EUR 1 billion, with additional Freedom House and ESG risk category screenings. Exhibits 2 and 3 show how these indices compare to the wider iBoxx Eurozone benchmark.

With a narrower issuer universe, the green bond strategy shows higher deviation in the country compositions compared to the iBoxx EUR Sovereigns ESG Tilted, narrowing issuers to eight countries. The index also exhibits higher yield with a higher duration exposure (see Exhibit 1).

Emerging Markets: Additional Measures

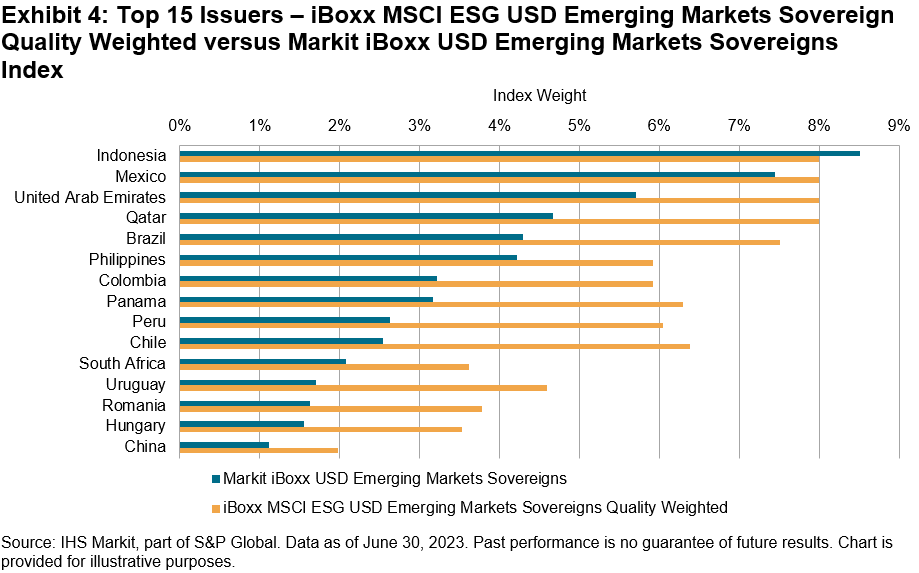

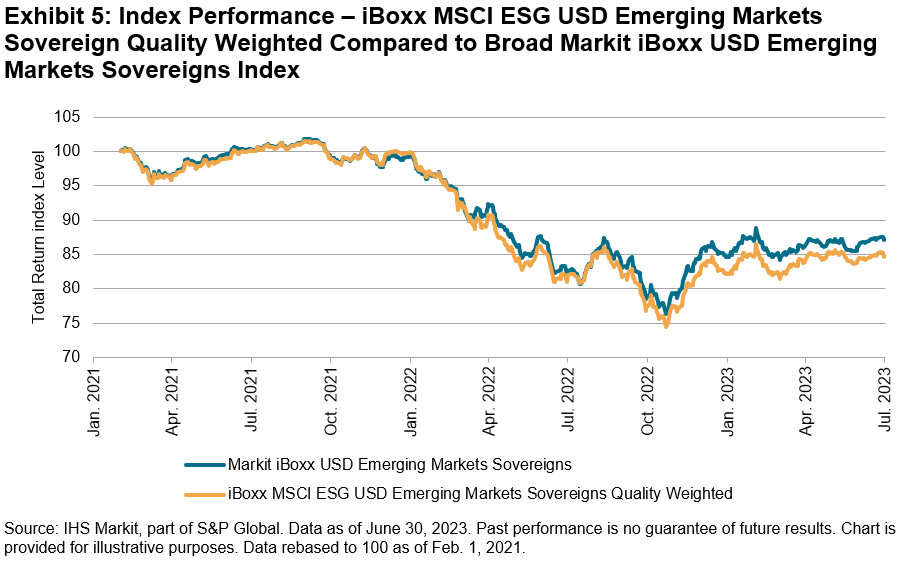

In addition to the above eurozone benchmarks, our sustainable indexing approach to emerging markets debt, the iBoxx MSCI ESG USD EM Sovereigns Quality Weighted Index, takes further fundamental metrics into consideration, in addition to a positive ESG score. These key criteria include GDP per capita, GDP growth trajectory, inflation, national debt and reserve levels, global competitiveness and the history of default. Given an increased number of parameters taken into consideration in the index construction, the index statistics and performance differ more notably from its broad benchmark, the Markit iBoxx USD Emerging Markets Sovereigns Index. The index weights shuffle substantially (see Exhibit 4) with the ESG version taking on slightly more duration (see Exhibit 1).

Conclusions

For index-based investing, the sustainability overlay in sovereign debt is likely to continue expanding and evolving. As the solutions continue to grow, they can borrow from the development of the corporate benchmarks, like ESG scores, impact investing or climate considerations metrics. However, it is important to recognize that the government debt category demands a distinct approach, with consideration of different criteria and construction methods. Amid the ongoing transitions in the sustainability landscape this year, the government debt ESG category will remain an interesting point of discussion for months to come.

1 Sustainalytics Country Risk Score.

The posts on this blog are opinions, not advice. Please read our Disclaimers.