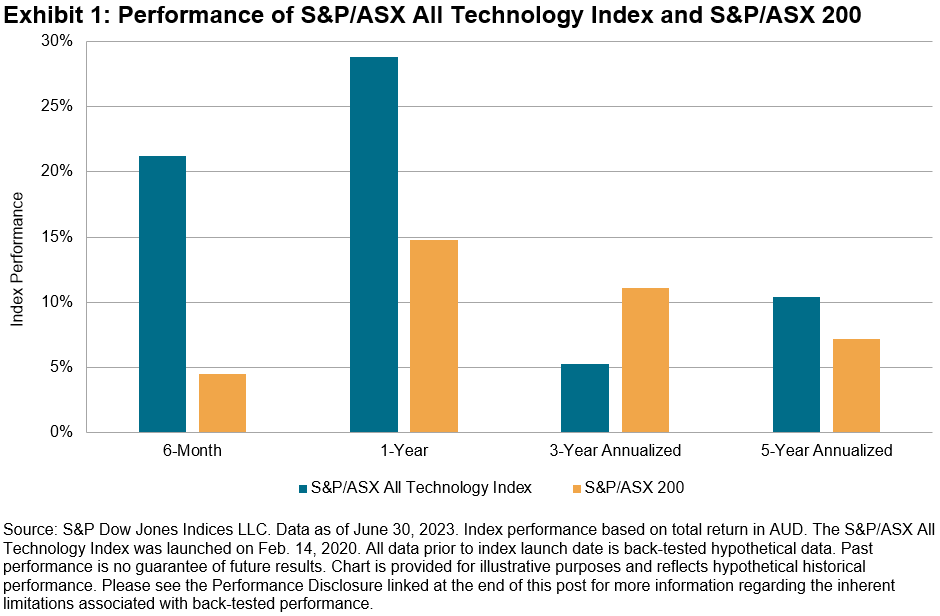

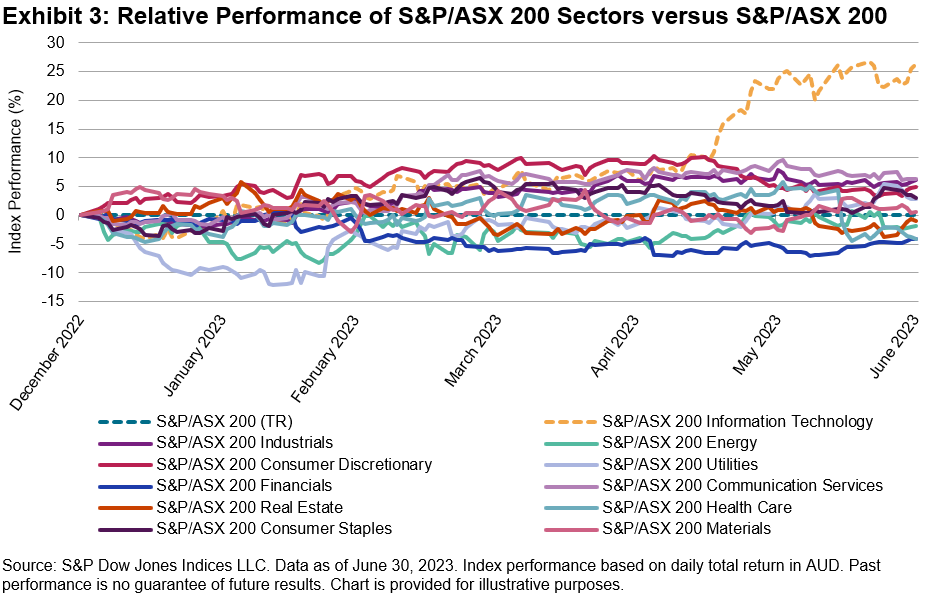

Following a poor 2022, the Information Technology sector has proven itself to be the outstanding performer in Australian equities in 2023. Despite rising interest rates, higher bond yields and weakening consumer confidence, market participants have still seen value in the Tech sector thus far in 2023. Tech’s turnaround has benefited the S&P/ASX All Technology Index, which has significantly outperformed the S&P/ASX 200 over the past 6 and 12 months.

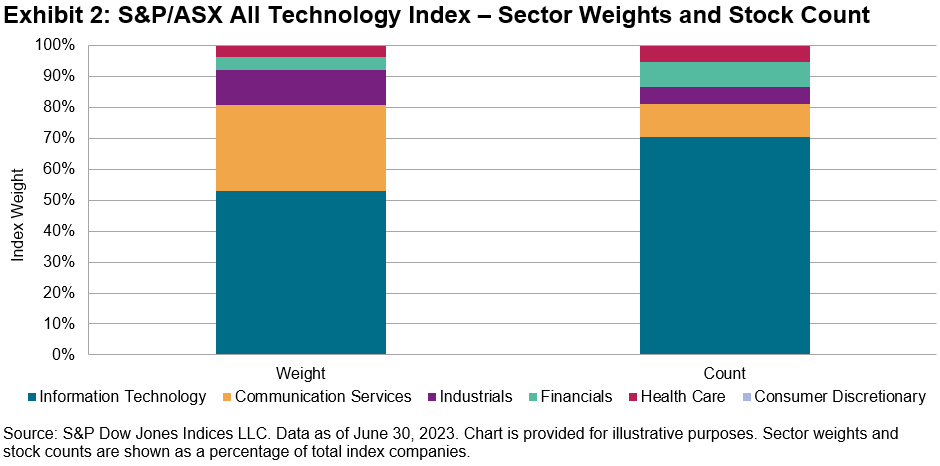

Launched in February 2020, the S&P/ASX All Technology Index provides representation to innovative technology-oriented companies across a broad range of sectors and industries. Currently comprising 37 companies, the index provides access to not just the Information Technology sector, but also to companies in specific sub-industries within the Health Care, Consumer Discretionary,1 Communication Services, Industrials and Financials sectors. Those sub-industries are Interactive Media & Services, Health Care Technology, Consumer Electronics, Data Processing & Outsourced Services and Transaction & Payment Processing Services.

Performance Drivers

Sector performance within the S&P/ASX 200 has been relatively clustered in 2023. The most notable outlier is the Information Technology sector, which surged ahead in Q2. Information Technology companies, along with those in Communication Services and Health Care sectors, are among the key contributors to outperformance for the S&P/ASX All Technology Index in 2023.

New Additions

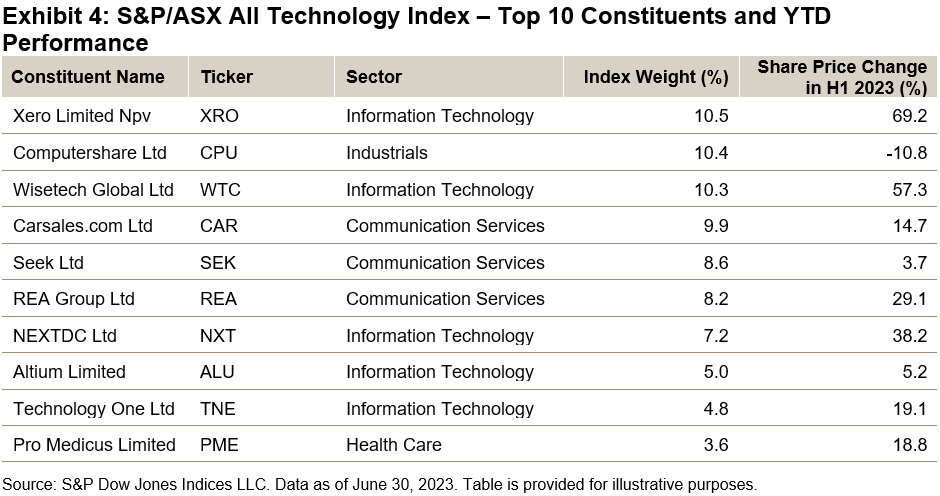

Two new companies were added to the S&P/ASX All Technology Index at the latest rebalance in June: Cogstate and FINEOS Corporation. Cogstate is classified in the Health Care Technology sub-industry and is involved in combining cognitive science expertise with digital innovations through clinical trials, healthcare and research. FINEOS Corporation is a software company providing modern customer-centric core software to the employee benefits and life, accident and health industry.

1 Note, there are currently no companies from the Consumer Electronics sub-industry of the Discretionary Sector eligible for index inclusion.

The posts on this blog are opinions, not advice. Please read our Disclaimers.