As the world continues to focus on sustainability and the energy transition, it is understandable that market participants are seeking to incorporate sustainability considerations into their commodities portfolios. To that end, on Feb. 23, 2023, S&P Dow Jones Indices (S&P DJI) launched the S&P GSCI Climate Aware, utilizing a new environmental dataset developed in collaboration with S&P Global Sustainable 1. It is the first broad-based commodity index in the market to incorporate environmental metrics.

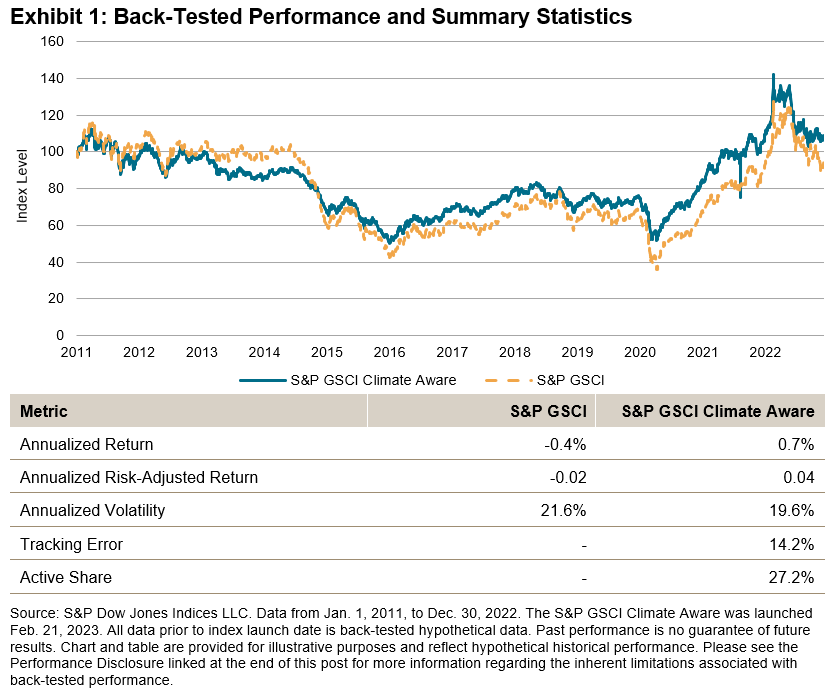

The S&P GSCI Climate Aware measures performance through futures of a long-only climate-aligned and climate-transition strategy across the constituents of the S&P GSCI. The index follows a portfolio optimization approach to compute constituent weights by seeking to reduce the environmental footprint of the index, while minimizing weight and sector deviations from the S&P GSCI. The optimized constituent weights are constrained to help maintain diversification, investability and liquidity for the index. The index seeks to achieve a 25% reduction in total environmental impact per dollar invested compared with the S&P GSCI, along with a 5% year-over-year decarbonization target, while maintaining total food production and ensuring land and water environmental impact per dollar invested are no higher than the S&P GSCI. Exhibit 1 provides back-tested performance and summary statistics for the index compared with the benchmark.

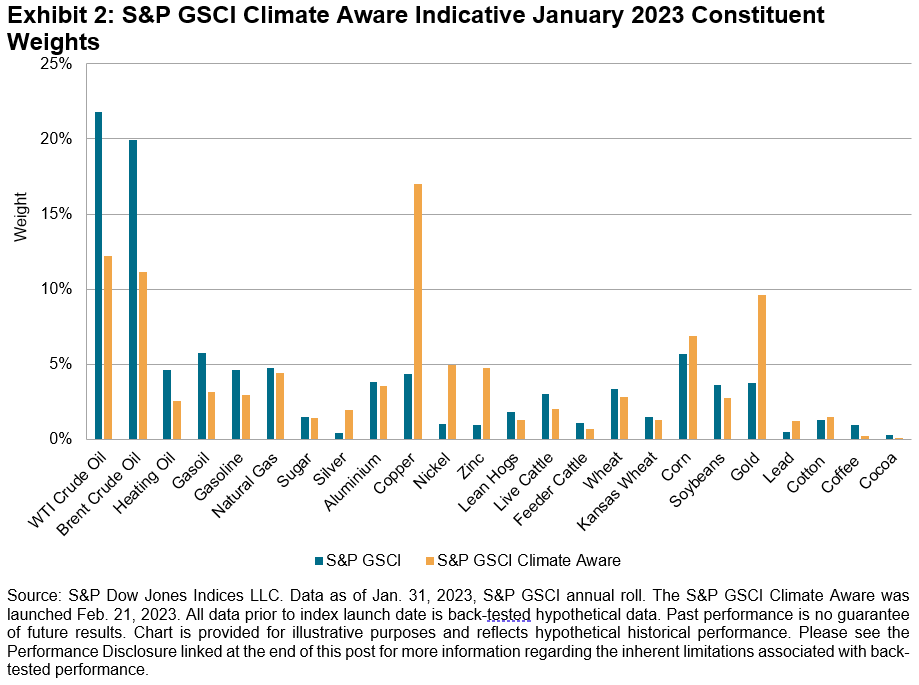

As environmental considerations come under the scope, market participants have expressed interest in maintaining diversified exposure to an inflation-sensitive asset in line with the benchmark S&P GSCI, while shifting allocations between commodities that may be substitutes, reflecting as closely as possible behaviors in the physical market that may be central to the transition. As such, the index redefines new commodity “sectors” to reflect the changing dynamics of the global economy, dividing the constituents into three economic sectors based on their impact on the environmental transition and currently available substitutions within each category: energy systems, food supply and other. As anticipated, the new index reallocates weights away from high-intensity fossil fuels to those metals important to the energy transition (see Exhibit 2).

The index utilizes a new set of environmental data—the S&P Global Commodity Environmental dataset—which provides physical and financial impact data on greenhouse gas emissions, water consumption and land use at the commodity level, based on life cycle impact assessment factors and natural capital valuation metrics. More information on the dataset can be found here.

S&P DJI continues to be the leader when it comes to bringing innovative, sustainability-focused index offerings to the market. The S&P GSCI Climate Aware is another example of how we look to drive transparency and incorporate sustainability criteria into our benchmark indices. To learn more, please visit the index webpage, or read about incorporating environmental considerations into commodities indices in our research paper published in February 2023.

The posts on this blog are opinions, not advice. Please read our Disclaimers.