At over 300 years old, the British government bond and stock markets are among the world’s oldest. They are also among the largest globally; ranked by float-adjusted market capitalization, the U.K. gilt market and U.K. stock market are the fourth and third biggest, respectively. The British investment industry has existed for centuries, with the country’s (and world’s) oldest collective investment scheme launched over 150 years ago. Despite this long history, U.K. investment funds have been just as likely to suffer from home country bias as their international peers.

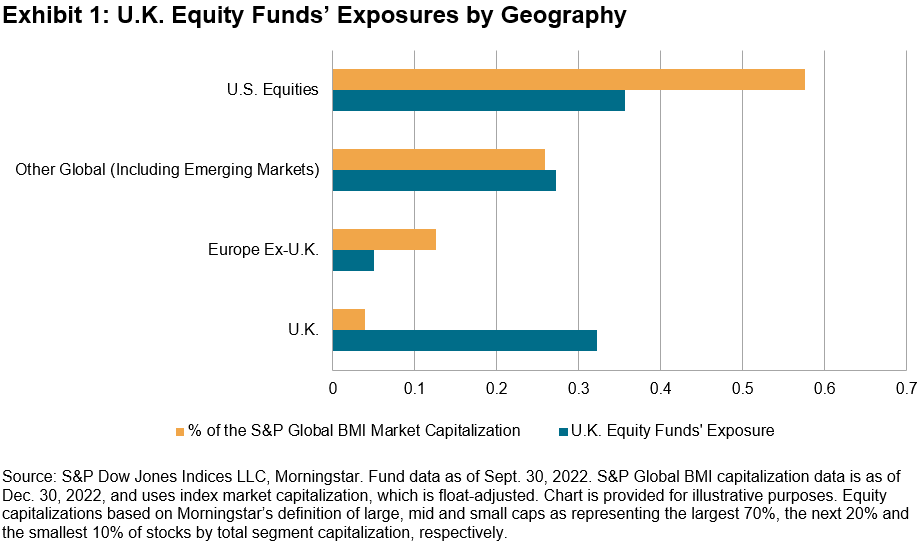

Exhibit 1 shows that U.K.-domiciled equity funds are substantially overweight their home market and underweight elsewhere, with the largest underweight in the U.S. By investing a disproportionate fraction of their assets in companies and industries based in their home country rather than globally, British market participants may be missing out on diversification benefits and potentially higher returns.

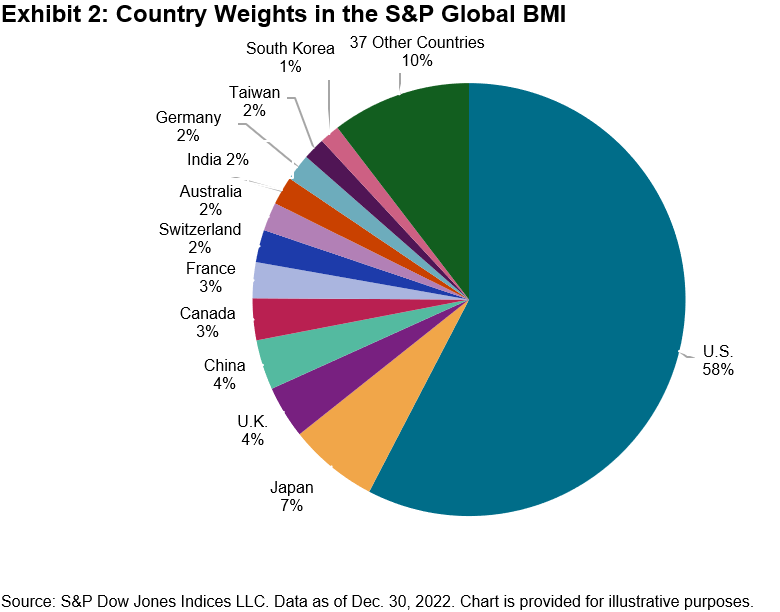

There is a large global opportunity set available to British investors, ranging across countries, sectors and currencies, and including large global companies without British equivalents. There were approximately 41,000 listed companies in the world at the end of 2019. Eliminating the smallest and least liquid names leaves around 14,000 companies from 25 developed and 24 emerging markets; Exhibit 2 shows how these compose the S&P Global BMI. With an aggregate free-float market capitalization of USD 66 trillion, the index is designed to reflect the global investable opportunity set. Given its 58% weight in the S&P Global BMI, for many investors the U.S. market represents the natural first step to globalizing their exposures.

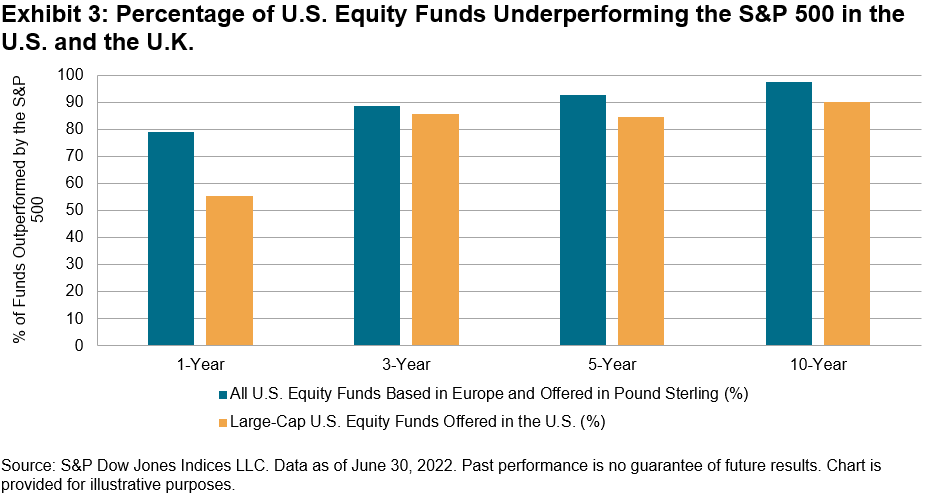

When considering an allocation to any market segment, including U.S. equities, investors must choose between active security selection and tracking a broad-based market portfolio. The SPIVA Europe Mid-Year 2022 and SPIVA U.S. Mid-Year 2022 Scorecards can help inform this decision. The historical data summarized in Exhibit 3 suggest that outperformance in large-cap U.S. equities is uncommon for fund managers based in either market, with outperformance even more elusive for longer time horizons.

These results are unsurprising. Simple arithmetic indicates that the average market participant earns the market return before fees and costs. Professional fund managers might expect to outperform in a market dominated by small retail traders, over whom they arguably have an informational and operational edge. But in markets dominated by large institutional and professional investors—as large-cap U.S. equities have been for at least 50 years—consistent outperformance becomes less likely, making the case for passive management stronger.

The posts on this blog are opinions, not advice. Please read our Disclaimers.