With inflation being a major issue in the current economy, consumers are increasingly looking for ways to combat their loss of purchasing power. One way to achieve this is to have sources of income that keep pace with, or even exceed, the inflation rate. Over the past four decades, dividends have played an increasing role as a source of income, growing from just 2.88% of all income in December 1981 to 6.25% of all income in March 2022.1

During inflationary periods, history has shown the importance of focusing on companies that have consistently increased dividends. A company’s ability to consistently increase dividends may signal a quality company that is able to continually generate increasing cash flows as well as high returns on capital.

Dividend Growers Methodology

In this blog, we will focus on the S&P U.S. Dividend Growers Index and S&P Global ex-U.S. Dividend Growers Index, which provide exposure to companies that have consecutively increased dividends for 10 and 7 years, respectively. In addition to the dividend policy filter, the top 25% of stocks ranked by indicated annual dividend yield are also excluded from these indices. This diminishes the risk of owning “yield traps,” or companies that have high dividend yields simply due to large stock price declines.

Dividend Growth Rate Outpaces the Inflation Rate over the Long Term

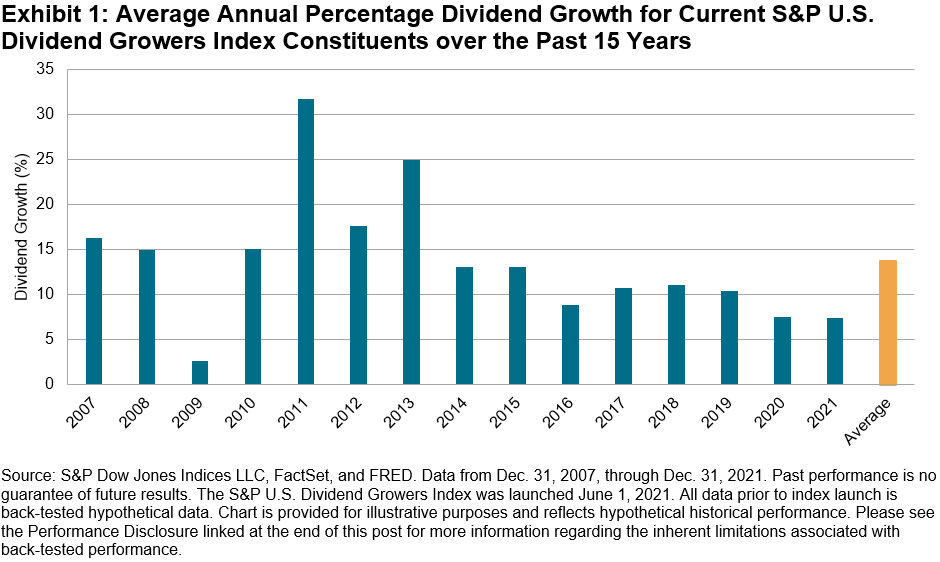

Exhibit 1 shows the average year-over-year annual percentage dividend growth rate for current S&P U.S. Dividend Growers Index constituents. The average year-over-year dividend growth rate over the past 15 years was 13.71%, surpassing the average year-over-year U.S. CPI rate of 2.21% over the same period.

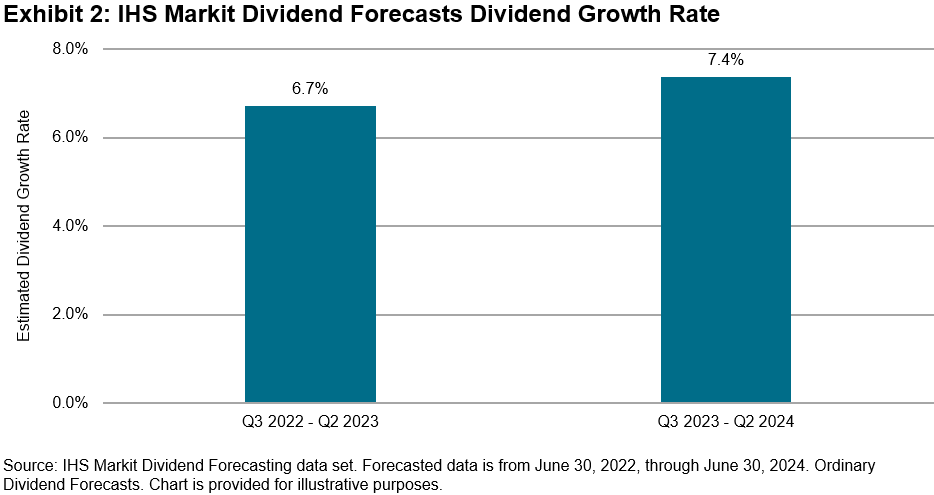

IHS Markit Forecasted Dividend Growth Rate

Exhibit 2 shows the year-over-year forecasted dividend growth rate for current S&P U.S. Dividend Growers Index constituents using the IHS Markit Dividend Forecasting data set.2 S&P Global’s Dividend Forecasting team provides discrete forecasts of the size and timing of dividend payments for over 30,000 stocks worldwide. Forecasts for stocks in the core Dividend Forecasting universe are generated by analysts using fundamental research, market announcements and unique quantitative insight. Over the next four quarters, forecasted dividend growth is expected to remain robust, at 6.7% year-over-year. The forecasted growth rate for the following four quarters (Q3 2023 to Q2 2024) is 7.4% year-over-year.

Performance During Inflationary Periods

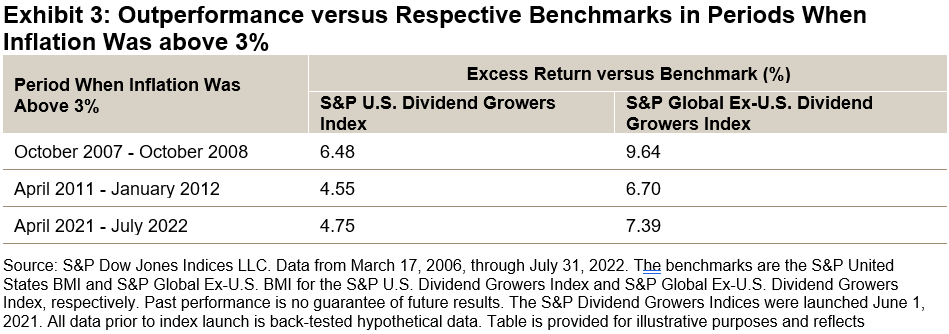

Exhibit 3 displays the outperformance of the S&P Dividend Growers Indices versus their respective benchmarks in periods when the year-over-year CPI rate exceeded 3% for at least six consecutive months. Both S&P Dividend Growers Indices significantly outperformed their benchmarks in the three most severe inflationary periods dating back to 2006.

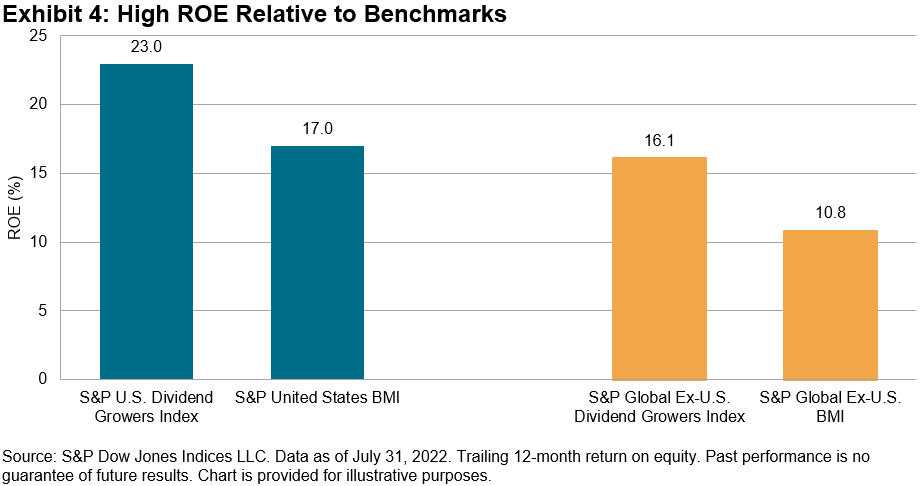

Exhibit 4 shows the trailing 12-month return on equity (ROE) for both S&P Dividend Growers Indices versus their respective benchmarks. The outperformance of the S&P Dividend Growers Indices during inflationary periods may be due to their substantially higher ROE. This is significant because companies that earn low returns on their capital can lose value in real terms, when the capital they invest earns a lower return than the inflation rate.

Full-Period Performance

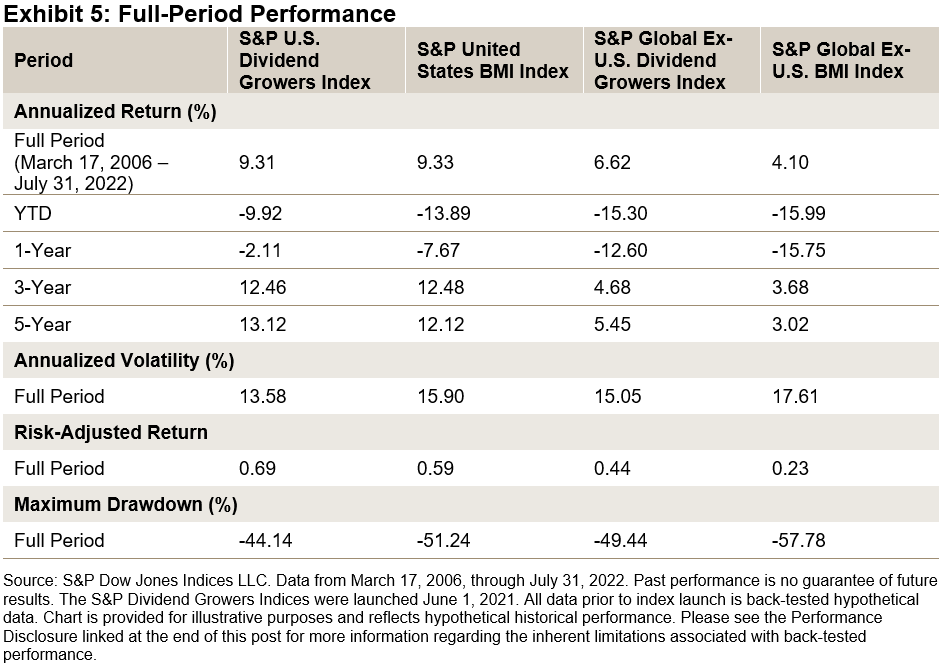

Exhibit 5 details the full-period performance comparison. Both S&P Dividend Growers Indices generated superior full-period risk-adjusted returns versus their benchmarks. Importantly, the S&P Dividend Growers Indices outperformed their benchmarks YTD as well as over the past year.

The S&P Dividend Growers Indices have historically outperformed their benchmarks on a risk-adjusted basis. Notably, they have significantly outperformed in recent inflationary periods, possibly due to their high-quality characteristics. Hence, the S&P Dividend Growers Indices may be a good option to consider if current inflation trends continue.

1 Source: Bureau of Economic Analysis. Data as of March 31, 2022.

2 See https://cdn.ihsmarkit.com/www/pdf/0822/IHS_Markit_Dividend_Forecasting_Methodology.pdf

The posts on this blog are opinions, not advice. Please read our Disclaimers.

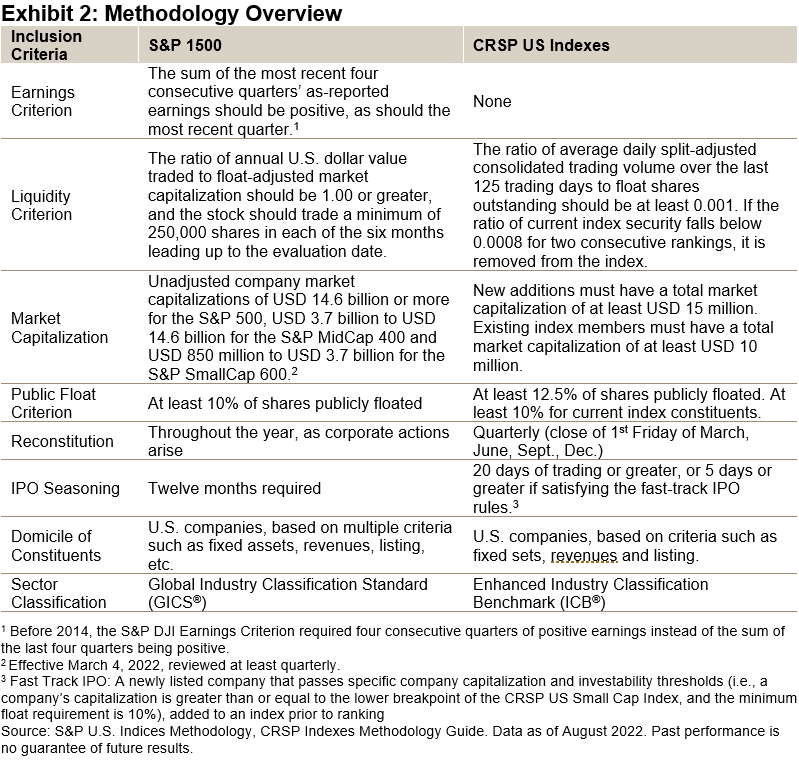

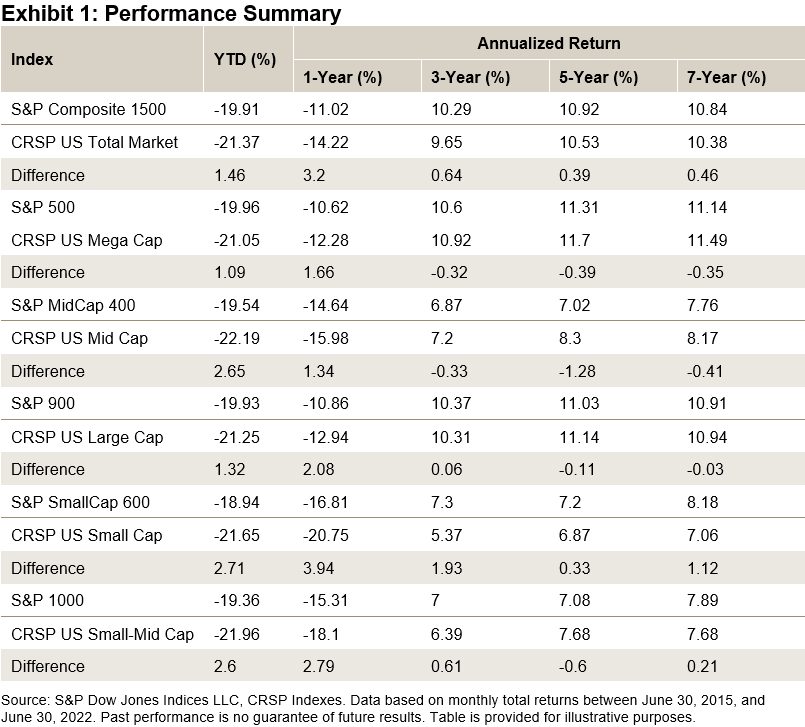

Differences in index construction can help us to understand these performance differentials. Exhibit 2 summarizes the methodologies underlying the S&P DJI U.S. equity indices and their CRSP counterparts. One of the biggest differences between the methodologies is that, unlike the CRSP indices, the S&P 1500 and its component indices use an earning screen: new index additions must have a history of positive earnings.

Differences in index construction can help us to understand these performance differentials. Exhibit 2 summarizes the methodologies underlying the S&P DJI U.S. equity indices and their CRSP counterparts. One of the biggest differences between the methodologies is that, unlike the CRSP indices, the S&P 1500 and its component indices use an earning screen: new index additions must have a history of positive earnings.