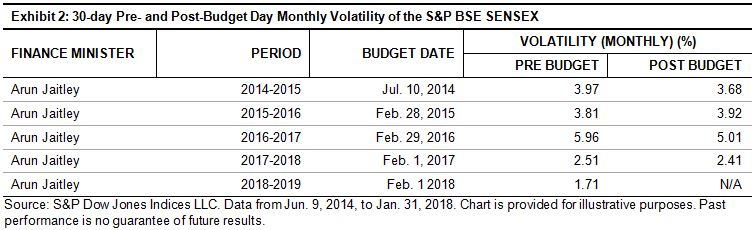

In November 2017, according to the Energy Information Administration, U.S. crude oil production surpassed 10 million barrels per day for the first time since November 1970. After 1970, it began to decline, dropping bellow 7 million barrels per day in February 1993, below 6 million barrels in March 1999, and then remaining at that level until November 2011, when it began steadily increasing.

How has the performance of crude oil futures contracts fared in comparison to crude oil production? The S&P GSCI Crude Oil was launched on May 1, 1991—with history dating back to 1987—to provide market participants with a reliable and publicly available benchmark for investment performance in the crude oil market.

Exhibit 1 depicts the performance of the S&P GSCI Crude Oil and the daily barrel production of U.S. crude oil from January 1987 until November 2017.

The two series had a negative correlation of 0.23 for the period studied and low or negative annual correlation, which implies that as overproduction and -supply occur in the market, futures prices tend to decline, a pattern that can be more clearly seen after September 2011.

Can increases or decreases in production be seen in the roll yield? The answer is yes and no. The roll yield or roll return, as measured by the excess return of the index minus the spot return, is the difference in the price of the expiring contract and the next eligible contract. Futures contracts expire on a regular basis, and futures-based indices must roll their positions into the next contract to maintain their exposure.

If a commodity’s forward price curve is downward sloping (in backwardation), then the roll process involves rolling into (buying) a futures contract that is trading cheaper than the current futures contract, hence a positive roll yield. However, if the commodity’s forward price curve is upward sloping (in contango), then the roll process would involve rolling into a futures contract that is trading at a higher price than the current futures contract, which results in a negative roll yield.

If the futures in the index are in backwardation regularly over time, and if the incidence of backwardation is higher relative to the degree of contango, then market participants tracking the indices will tend to profit from the roll process.

Analyzing the S&P GSCI Crude Oil roll return for the period between January 1987 and November 2017 (a total of 370 observations) showed that during this period, daily oil production increased or decreased relatively equally. The roll yield appeared more sensitive to declines in production, resulting in a negative yield almost 60% of the time, while an increase in production only resulted in a positive roll yield 43% of the time, implying that shortages or undersupply in the market was more likely to drive up prices than oversupply to weigh down on futures prices. That is likely because crude oil prices are sensitive to factors other than production, such as geopolitical risk and inventory levels.

The posts on this blog are opinions, not advice. Please read our Disclaimers.