When I was a teenager growing up in Basel, I witnessed first-hand one of the events that put sustainability thinking on the agendas of the corporate landscape. On November 1, 1986, I was woken up by loud sirens. A disastrous fire had broken out at a chemical plant warehouse. Over 1,000 tons of agrochemical product and quicksilver had caught fire. The fire department was quick to contain the fire, but the water it used to extinguish it flowed into the Rhine. Overnight, the contaminated water turned the river a bright red color and caused unprecedented fish mortality.

Events such as these brought awareness of business risks, predominantly environmental risks, to the fore. Sustainability thinking had landed on the agendas of corporate executives!

Initially, it assumed a narrow interpretation of risk-management pertaining to environmental aspects. In other words, it was purely focused on what needs to be done to prevent operating licenses being revoked. However, over time, corporations began to see and enjoy the broader set of business opportunities that integrating sustainability practices more deeply can unlock. It is no wonder that the number of companies that actively participate in our Corporate Sustainability Assessment (CSA), an annual ESG analysis of over 3,900 listed companies, in order to secure a spot in the coveted Dow Jones Sustainability Indices, has continued to increase over the years.

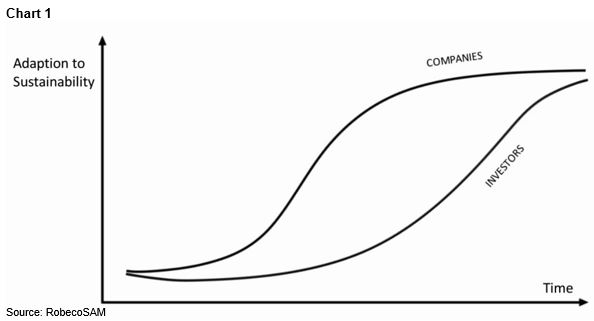

Gradually, and with somewhat of a time-lag, sustainability thinking spread from the corporate sector to the investor community (see Chart 1). Despite this, the way in which the financial sector has embraced sustainability follows a very similar pattern to that of the corporate world.

When investors began to address the challenge of sustainability, the predominant focus was on risk management. Sound familiar? Specifically, they were focused on avoiding controversial investments. Exclusions were the natural answer, but in time and in much the same way as it happened in the corporate sector, this preliminary sustainability thinking evolved. The opportunities that come along with a deeper integration of sustainability principles now also became obvious to investors: identifying more innovative business models, attractive investments, better performance, to name a few. And while exclusionary screening is still the most widely applied Sustainability Investing strategy, more sophisticated strategies are rapidly gaining traction (see Chart 2).

Source: 2016 Global Sustainable Investment Review

Today, some say that integration of ESG in finance has become mainstream. Certainly, leaps and bounds toward a more sustainable approach to business have been made, but we have not yet reached a point where sustainability principles have permeated all the norms, be it in finance or in other sectors. That is the beacon we must continue to strive towards and we must be patient, persistent and rigorous in our endeavor.